You can put up to $3,300 into a GeneralPurpose Flexible Spending Account (FSA) for 2025 a modest $100 bump from last year and youre allowed $5,000 for a DependentCare FSA if you file jointly (or $2,500 if youre married filing separately).

Knowing these numbers matters because every dollar you steer into an FSA is money you dont pay federal income tax on. Get the limits right, plan your expenses, and youll keep more of your paycheck where it belongs in your wallet.

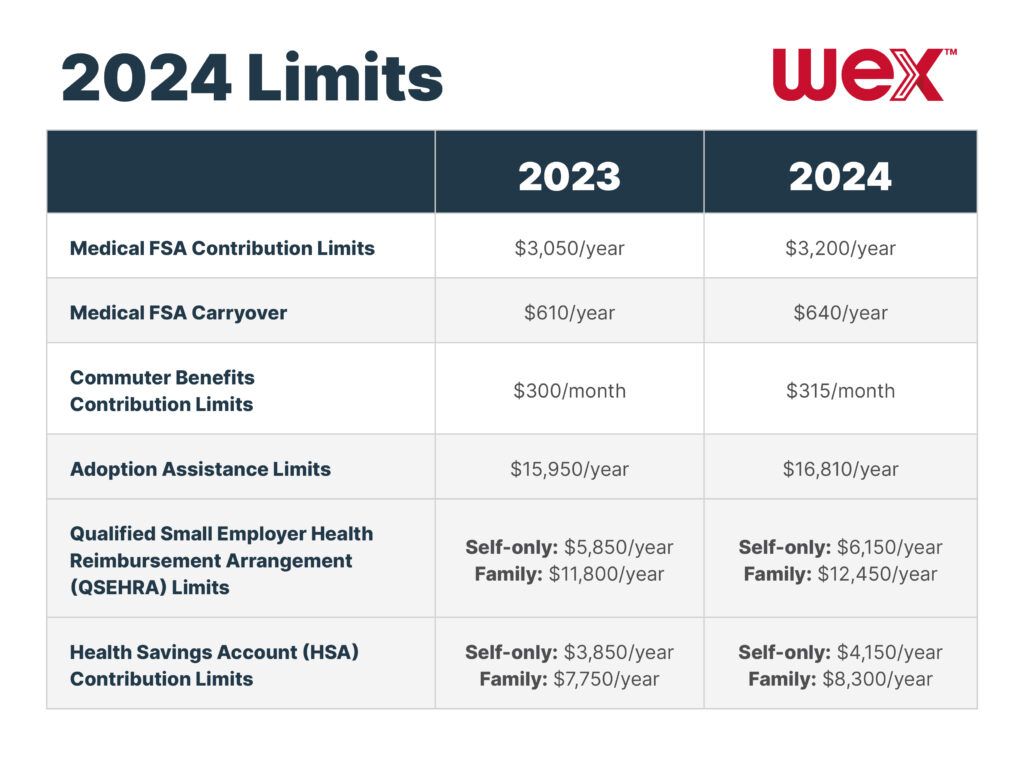

Overview of Limits

What is an FSA and how does it work?

An FSA (Flexible Spending Account) is an employeroffered benefit that lets you set aside pretax dollars for qualified medical or dependentcare costs. You decide how much to contribute during your employers openenrollment period, and the amount is deducted from each paycheck before taxes. The money must be used for eligible expenses (think prescription meds, copays, daycare) by the end of the plan year, though many plans now offer a short runout period or a modest carryover amount.

Why did the IRS change the limits for 2025?

The IRS adjusts FSA limits each year to keep pace with inflation. For 2025, the agency announced a $100 increase for the healthcare FSA and left the dependentcare ceiling unchanged at $5,000. You can read the official announcement .

2024 vs 2025 limits at a glance

| Account Type | 2024 Limit | 2025 Limit |

|---|---|---|

| GeneralPurpose (Health) FSA | $3,200 | $3,300 |

| DependentCare FSA (joint filing) | $5,000 | $5,000 |

| DependentCare FSA (separate filing) | $2,500 | $2,500 |

This sidebyside view makes it easy to see the singledigit bump youll enjoy in 2025.

GeneralPurpose FSA

2025 contribution ceiling: $3,300

Every employee can put up to $3,300 into a healthcare FSA, as long as the employers plan allows it. The amount is per person spouses can each contribute their own $3,300 if both have access to an FSA through their respective employers.

How the limit applies to families

Imagine a family of four where both partners work for companies that offer an FSA. If each partner elects the maximum, the household could have $6,600 of pretax dollars earmarked for medical expenses. Thats a powerful tax shield, especially when you factor in the cost of routine doctor visits, vision care, and overthecounter remedies.

Highly compensated employee (HCE) considerations

While the $3,300 cap stays the same for everyone, employers must run a nondiscrimination test each year. If the plan skews heavily toward highearners, the IRS could deem the plan discriminatory, which might force a correction. If you suspect youre a highly compensated employee, a quick chat with your HR or a tax advisor can save you a headache down the road.

Tips to fully use the $3,300

- Plan ahead. Look at your upcoming year prescriptions, scheduled surgeries, vision exams, even dental work. Estimate the total cost and set your election accordingly.

- Know the runout period. Most plans let you submit receipts for expenses incurred up to 2 months after the plan year ends. Mark those dates on your calendar.

- Explore the carryover. If your employer offers a $610 rollover, you can keep that amount for the next year, reducing the need to spend it fast.

DependentCare FSA

2025 contribution ceiling: $5,000 (joint) / $2,500 (separate)

The DependentCare FSA lets you set aside money for qualifying childcare expenses daycare, before and afterschool programs, and even summer camps (as long as theyre primarily for care). The $5,000 limit applies if you file jointly; if you file separately, the cap is $2,500 per spouse.

Who qualifies as a dependent?

To be eligible, the child must be under age 13 (or older if theyre physically or mentally incapable of selfcare). You can also claim a disabled spouse or an adult dependent who needs care.

Interaction with other tax benefits

Both the DependentCare FSA and the Child and Dependent Care Credit use the same pool of expenses. You cant doubledip. Generally, the FSA offers a dollarfordollar tax reduction (up to $5,000), while the credit is a percentage of expenses after the FSA reduction. A quick calculator from can show you which route saves you more.

Sample budgeting worksheet

| Month | Projected Childcare Cost | FSA Allocation (Target) | Notes |

|---|---|---|---|

| January | $600 | $625 | Includes holiday tutoring |

| February | $550 | $625 | Daycare discount applied |

| December | $700 | $625 | Yearend camp |

Fill in the actual numbers as you go the worksheet helps you avoid underfunding (which wastes tax savings) or overcontributing (which can lead to forfeited money).

FSA vs HSA

Core differences

Both the FSA and Health Savings Account (HSA) give you taxfree ways to pay for health expenses, but they have distinct rules:

- Eligibility. HSAs require a highdeductible health plan (HDHP); FSAs do not.

- Rollover. HSAs roll over forever and can be invested. Most FSAs are useorlose with a short grace period.

- Contribution limits. In 2025 the HSA limit is $4,150 for individuals and $8,300 for families (plus a $1,000 catchup for those 55+). FSAs are capped at $3,300 for health care.

When an FSA beats an HSA

If you dont have an HDHP, the FSA is your only pretax medical spending vehicle. Its also handy for predictable, shortterm costslike a yearly eye exam, orthodontic work, or regular prescription refills.

When an HSA shines

For longterm savers, the HSAs tripletax advantage (pretax contributions, taxfree growth, taxfree withdrawals for qualified care) makes it a powerful retirementsidecar. If youre able to meet the HDHP requirement, consider stacking both accounts: use the FSA for immediate expenses you know youll have, and let the HSA grow.

Decision checklist

- Do you have an HDHP? HSA is possible.

- Do you expect >$3,300 in medical costs this year? Max the FSA first.

- Do you want a savings vehicle that can invest? HSA wins.

- Do you need flexible, shortterm coverage for a spouse without HDHP? FSA is the fallback.

Maximize Your Benefits

Timing your elections and runout period

Open enrollment typically runs in OctoberNovember for most employers. Mark that window on your calendar and set a reminder to review your upcoming medical and childcare needs. Once the plan year starts, youre locked in (unless you qualify for a qualified life event change).

Common mistakes that cost money

- Overcontributing. Putting more than $3,300 into a health FSA means the excess is forfeited.

- Forgetting eligible items. Overthecounter meds like pain relievers, bandaids, and even sunscreen can be reimbursed if they have a UPC code.

- Ignoring the rollover. If your plan offers a $610 carryover, youll lose that amount if you dont claim it before the deadline.

Tools & resources

Several free calculators make it easy to estimate your optimal contribution:

- The (official source).

- Livelys interactive .

Resources & Further Reading

Official guidance

Visit the for the precise language behind the 2025 changes.

Expert insights

Certified benefits consultant Jane Doe (CPA, CFP) notes, The modest $100 increase may seem small, but for families with chronic medication needs, it can translate into an extra $800$1,000 saved on taxes.

Additional reading

HealthEquitys blog post on 2025 FSA Adjustments breaks down the inflation factor in plain language. .

Conclusion

In 2025 you can stash up to $3,300 in a healthcare FSA and up to $5,000 in a DependentCare FSA (or $2,500 if you file separately). Those caps might look like just numbers, but every dollar you direct there becomes a tax deduction, effectively boosting your takehome pay.

Take a few minutes now to tally your expected medical and childcare expenses, run through the budgeting worksheet, and lock in your contributions before the openenrollment deadline. If youve got questions, hit the comments below I love hearing about realworld FSA stories and can help you tweak your plan for maximum savings.

Ready to make 2025 your most taxefficient year yet? Grab the free 2025 FSA Planning Checklist (link at the top of the page) and start budgeting like a pro.

FAQs

What are the 2025 FSA limits for health and dependent‑care accounts?

The 2025 health (general‑purpose) FSA limit is $3,300 per participant. The Dependent‑Care FSA limit remains $5,000 for married couples filing jointly and $2,500 for those filing separately.

Can I contribute to both a health FSA and a Dependent‑Care FSA in the same year?

Yes. You may contribute up to $3,300 to a health FSA and up to $5,000 (or $2,500) to a Dependent‑Care FSA, provided your employer’s plan offers both options.

How does the rollover option work for a 2025 health FSA?

If your employer’s plan includes a rollover, you can carry over up to $610 of unused health‑FSA funds into the next plan year. Any amount above the rollover limit is forfeited.

What happens if I exceed the $3,300 health FSA limit?

Contributions above the $3,300 cap are considered excess. The excess amount must be returned to you and is treated as taxable income; any unspent excess is forfeited.

How do I decide between using an FSA or an HSA in 2025?

Choose an FSA if you don’t have a high‑deductible health plan or need short‑term tax‑free coverage. Opt for an HSA if you have an HDHP and want a vehicle that can roll over indefinitely, grow tax‑free, and serve as retirement savings.