At first, I thought insurance cost share was just another buzzword you hear on a webinar and then forget about. Turns out, its the piece of the puzzle that decides whether youre paying a tiny copay at the pharmacy or getting hit with a surprise bill after a trip to the ER. In short, insurance cost share is the portion of your medical expenses you pay yourselfusually through deductibles, copays, and coinsurance. Knowing how it works can save you from nasty financial shocks and help you pick a plan that actually fits your life.

CostShare Basics

What does cost share mean in health insurance?

Think of healthinsurance cost share as the splitting the bill part of a dinner with friends. The insurer covers a big chunk, but youre still on the hook for a slice. That slice shows up in three main flavors:

- Deductible: The amount you must pay outofpocket before the insurer kicks in.

- Copayment (or copay): A fixed dollar amount you pay for a specific service, like $20 for a primarycare visit.

- Coinsurance: A percentage of the cost you pay after the deductible is met, such as 20% of a specialists fee.

These three pieces together form the insurance cost share. Theyre the numbers youll see in the Summary of Benefits section of any plan brochure.

Realworld example: Janes $3,000 deductible vs. $500 copay

| Plan Feature | Janes Plan |

|---|---|

| Deductible | $3,000 |

| Copay (Primary Care) | $30 per visit |

| Coinsurance | 20% after deductible |

| OutofPocket Maximum | $5,000 |

Jane pays the first $3,000 of her medical costs. After that, each doctors visit costs her $30, and she chips in 20% of any larger bills until she hits $5,000 total outofpocket.

What is cost share in other contexts (grants, Medicaid, etc.)?

Costshare isnt exclusive to health insurance. Nonprofits often have to contribute a portion of a grants total budgetthis is called a grant cost share. Medicaid programs also have costshare rules, where beneficiaries might cover a small part of services. While the numbers differ, the principle stays the same: youre sharing the financial responsibility.

Minicase study: A nonprofits 30% grant costshare

Imagine a charity receiving a $100,000 federal grant that requires a 30% costshare. The organization must contribute $30,000 of its own fundsmaybe from fundraising or existing reservesto qualify. This shows that costshare concepts can appear in many financial landscapes, not just health insurance.

Types of CostSharing

Deductibles: The firstpay hurdle

Deductibles are that initial mountain you have to climb before the insurer says, Alright, weve got you. Highdeductible health plans (HDHPs) often come with lower monthly premiums, which can be tempting if youre healthy and dont expect many doctor visits. But if youre prone to chronic conditions, a big deductible can feel like a financial swamp.

Comparison chart: $500 vs. $2,000 deductible scenarios

| Scenario | Annual Premium | Deductible | OutofPocket Max |

|---|---|---|---|

| Low Deductible | $5,200 | $500 | $3,000 |

| High Deductible | $3,800 | $2,000 | $5,000 |

If you rarely see a doctor, the highdeductible plan could save you $1,400 a year in premiums. But be ready for that $2,000 bill if something unexpected pops up.

Copayments: Fixedamount stopgap payments

Copays are the ticket price you pay each time you use a service. Theyre predictable and help you budget. A typical primarycare copay might be $20$30, while an ER visit could be $150$200.

Sample copay schedule for a best costsharing health insurance plan

| Service | Copay |

|---|---|

| Primary Care Visit | $25 |

| Specialist Visit | $40 |

| Urgent Care | $60 |

| Emergency Room | $180 |

| Prescription (generic) | $10 |

These flat fees make it easy to know ahead of time exactly what youll owe at the checkout.

Coinsurance: Percentagebased sharing

Coinsurance steps in after youve met your deductible. If your plan says 20% coinsurance, youll pay 20% of the allowed amount for each service, and the insurer pays the remaining 80%.

Example calculation: 20% coinsurance on a $1,200 procedure

Deductible already met. Procedure cost = $1,200. You pay 20% $240. Insurer pays $960. Simple arithmetic, but it can add up quickly if you have multiple highcost procedures.

Is cost share the same as coinsurance?

Nope. Coinsurance is just one slice of the larger costshare pie. Think of cost share as the umbrella term that covers deductibles, copays, and coinsuranceall the ways you share the bill with your insurer.

CostSharing Reductions

What is a costsharing reduction in health insurance?

CostSharing Reductions (CSRs) are subsidies that lower your deductible, copays, and coinsurance if you enroll through the Health Insurance Marketplace and meet certain income thresholds. According to , CSRs are available to households earning between 100% and 250% of the federal poverty level.

CSR benefit table: How much you could save

| Income Level | Deductible Reduction | Copay Reduction | Coinsurance Reduction |

|---|---|---|---|

| 100150% FPL | $1,200 | $15 | 5% |

| 151200% FPL | $800 | $10 | 3% |

| 201250% FPL | $400 | $5 | 1% |

If you qualify, those reductions can transform a $3,000 deductible into a $1,800 onemaking a huge difference in a medical emergency.

Pros & Cons

Benefits of costshare designs

Lower premiums are the most obvious perk. By agreeing to shoulder some costs, insurers can offer plans that dont drain your bank account each month. Costshare also nudges people to use medical services more wiselyno one wants to pay a $30 copay for a cold that will clear up on its own.

Risks & hidden costs

On the flip side, costshare can bite you when you least expect it. A high deductible may seem harmless until you need an MRI, and suddenly youre looking at a $2,500 bill. Limited provider networks, surprise balancebilling, and priceshocking emergencies can also make the outofpocket amount feel like a cliff dive.

Reallife anecdote: Toms surprise ER bill

Tom thought his $150 monthly premium was a win. Two weeks later, a slip on ice sent him to the ER, and his plans $500 deductible kicked in. Add a $250 copay, and the total bill hit $2,000far beyond what he expected. Toms story reminds us why understanding the full costshare picture matters more than the premium alone.

Choosing the Right Plan

Questions to ask yourself before selecting a plan

Before you click Enroll, pause and consider:

- How much can you comfortably pay outofpocket each year?

- Do you have chronic conditions that need regular visits or prescriptions?

- Do you prefer predictable copays or are you okay with a high deductible for lower premiums?

- Will you qualify for a CSR or other subsidies?

Decisiontree checklist (visual aid suggestion)

Imagine a flowchart that starts with Do you expect frequent medical visits? If yes, you might lean toward a lowdeductible plan with modest copays. If no, a highdeductible plan with a healthsavings account (HSA) could be smarter. You can sketch this on a piece of paper or use a free online tool to map your options.

Tools & resources for comparing costshare structures

Many reputable sites let you filter plans by deductible, copay, and coinsurance. The is a solid start, and the MetLife CostSharing Guide breaks down each component with realworld numbers. Using these tools, you can see at a glance which plan aligns with your budget and health needs.

Conclusion

Insurance cost share isnt just a wall of numbers; its the mechanism that decides how much you pay today versus what the insurer covers tomorrow. By grasping deductibles, copays, coinsurance, and possible costsharing reductions, you can avoid surprise bills, choose a plan that fits your lifestyle, and feel confident that youre not leaving money on the table. Take a moment now to run a quick costshare calculator on the Marketplace, download the decisiontree checklist, and share your own experiences in the commentsyour story could help the next reader dodge a financial pothole.

FAQs

What exactly is an insurance cost share?

It is the portion of your healthcare expenses that you pay out‑of‑pocket, typically through a deductible, copayment, or coinsurance, while your insurer covers the rest.

How do deductibles, copays, and coinsurance differ?

A deductible is the amount you must pay before coverage starts. A copay is a fixed fee for a specific service (e.g., $25 for a doctor visit). Coinsurance is a percentage of the cost you pay after the deductible is met.

Can I lower my cost share with subsidies?

Yes. If you enroll through the Health Insurance Marketplace and your household income is between 100 % and 250 % of the federal poverty level, you may qualify for Cost‑Sharing Reductions (CSRs) that lower deductibles, copays, and coinsurance.

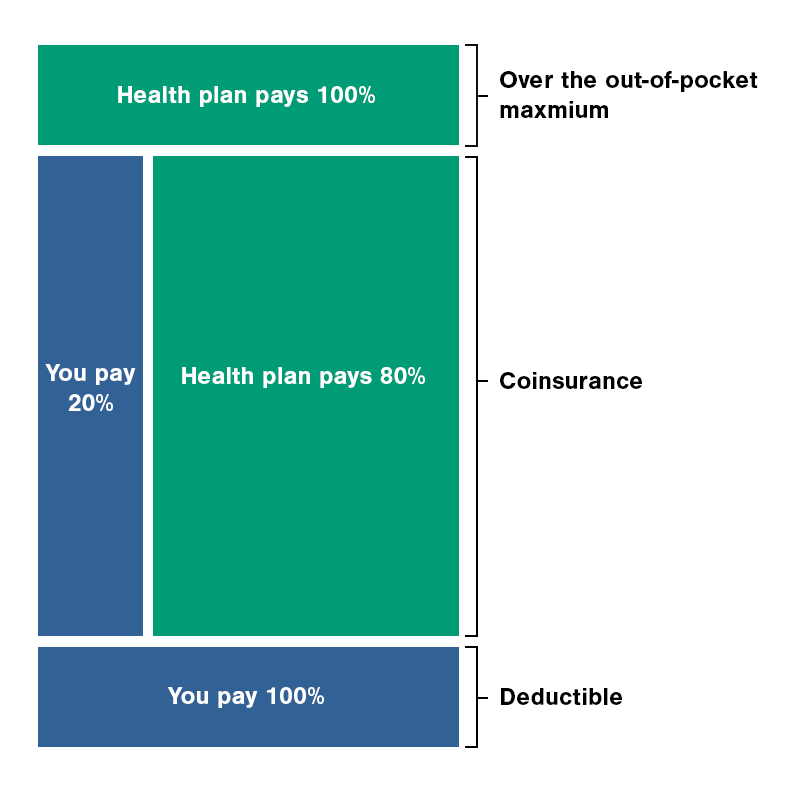

What happens after I reach my out‑of‑pocket maximum?

Once you hit the out‑of‑pocket maximum, the insurance company pays 100 % of covered services for the rest of the plan year, eliminating additional cost‑share costs.

How should I choose a plan based on cost share?

Consider your health needs, budget for unexpected expenses, and whether you qualify for subsidies. Low‑deductible plans with modest copays suit frequent users, while high‑deductible plans paired with an HSA can save money for those who expect few medical visits.