A copayment amount is the fixed dollar fee you drop in the cash register every time you get a covered healthcare service think $20 for a routine doctor visit or $10 for a prescription. Its the piece of the bill youre on the hook for, right after any deductible is satisfied.

Understanding that little number can be a gamechanger for your budget, because it tells you exactly how much youll owe before the insurance company steps in. No guessing, no surprise bills just a clearcut amount you can plan for each time you need care.

The Basics

What Exactly Is a Copay?

A copay (or copay) is a set amount you pay per service. Unlike a percentage or a sliding scale, the number never changes no matter how pricey the visit is. For example, if your plan says a primarycare visit costs a $30 copay, you hand over $30 whether the doctor bills $150 or $300.

Quick Example

Imagine youve just finished a flu shot at a pharmacy. The receipt flashes Copay $10. Even if the pharmacys list price for the vaccine is $45, you only pay the $10 because thats your copayment amount for preventive care.

How Is the Copayment Amount Displayed?

Most insurers print the copay right on your member ID card look for a row that says Primary Care $25 or Specialist $40. Youll also see it in your online portal under Plan Details, and on the Explanation of Benefits (EOB) after a visit.

According to Cignas FAQ, the amount is usually highlighted in bold so members can spot it quickly.

RealWorld Peek

Jane, a 34yearold graphic designer, once thought her insurance covered an entire specialist visit. A quick glance at her ID card revealed a $45 copay for specialists. She paid it at the front desk and walked out with a clear bill no hidden fees.

When Do You Pay the Copay?

Most of the time you pay the copay at the point of service right when you check in at the doctors office or when the pharmacist rings up your prescription. Some plans let you settle later through an online portal, but the rule of thumb is: youll see that amount before the service is completed.

Exceptions to the Rule

- Telehealth visits may be billed after the call.

- Innetwork hospitals sometimes send the copay to your billing address a few days later.

- Some employersponsored plans waive the copay for preventive services you pay $0.

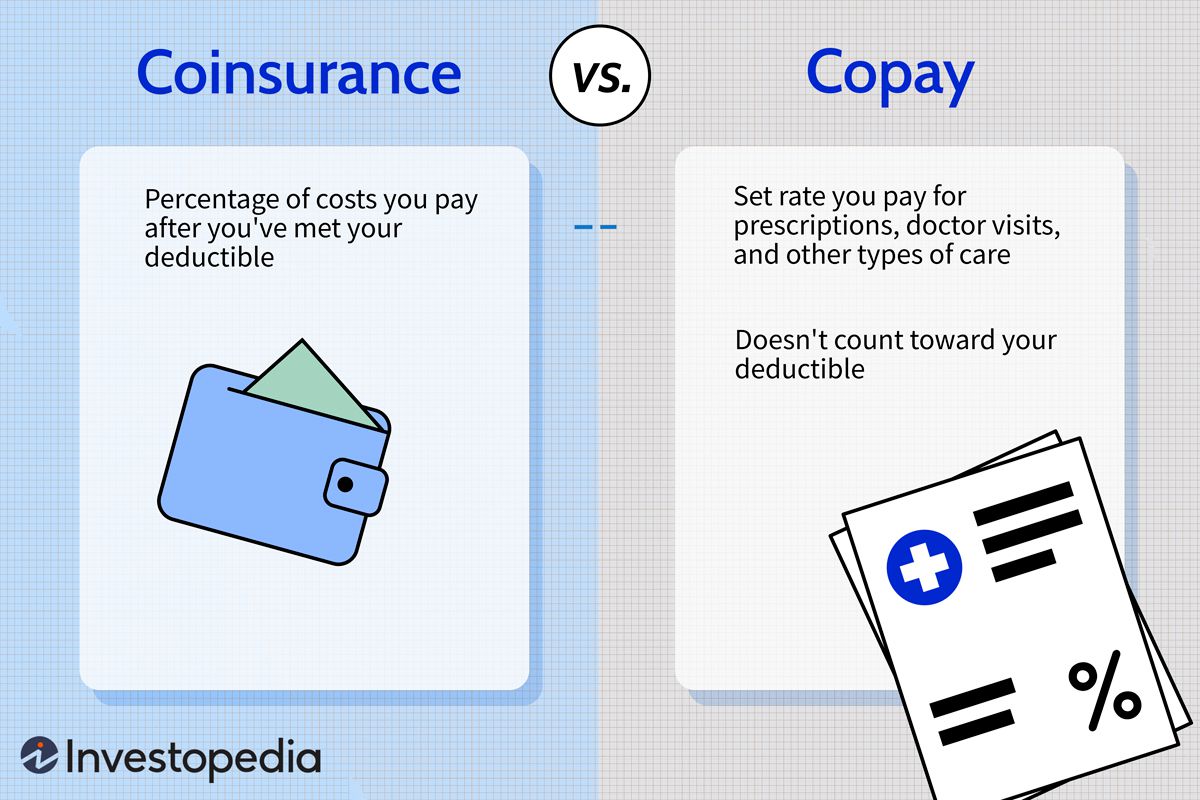

Copay vs

Copay vs Deductible

A deductible is the amount you must pay outofpocket before the insurance starts to share costs. Think of it as the entry fee to the healthcare club. Once that fee is met, the copay kicks in for each subsequent visit.

Copay vs Coinsurance

Coinsurance is a percentage of the allowed charge (e.g., 20%). If a lab test costs $200 and your coinsurance is 20%, youd pay $40. A copay, on the other hand, stays the same $30, $40, or whatever your plan says no matter the tests price tag.

Copay vs OutofPocket Maximum

Every dollar you spend on deductibles, copays, and coinsurance adds up toward your annual outofpocket maximum. When you hit that cap, the insurance covers 100% of any additional covered services for the rest of the year.

Comparison Table

| Term | What You Pay | When You Pay | Typical Example |

|---|---|---|---|

| Deductible | Fixed total amount | First dollars of the year | $1,200 before any coverage |

| Copay | Fixed amount per service | Each visit/prescription | $25 for a primarycare visit |

| Coinsurance | Percentage of allowed charge | After deductible met | 20% of a $300 lab test = $60 |

| OutofPocket Max | Cap on total costsharing | End of plan year | $5,000 limit |

How It's Set

Factors Insurers Consider

Insurers look at several moving parts when they decide your copayment amount:

- Service type: Primary care, specialist, ER, urgent care, or pharmacy each gets its own tier.

- Plan design: HMOs tend to have lower copays than PPOs, while highdeductible plans may replace copays with higher coinsurance.

- Provider contracts: Negotiated rates with doctors and hospitals shape the flat fee youll see.

Common Copay Ranges (20242025)

While exact numbers vary, most plans fall within these bands:

- Primary care: $10$30 per visit

- Specialist: $25$50 per visit

- Emergency department: $100$250 per visit

- Prescription (generic): $5$15

- Prescription (brand): $20$50

Why Some Copays Are Waived

Many insurers temporarily waive copays for certain services think flu shots, COVID19 tests, or annual wellness exams. The idea is to remove financial barriers for preventive care.

Case Study UnitedHealthcare Copay Waivers

UnitedHealthcare announced that, for the 2024 plan year, most preventive services like mammograms and annual physicals have a $0 copay. The policy, detailed on the UnitedHealthcare website, aims to encourage members to stay on top of health checks without worrying about extra costs.

Common Questions

What Is a Copay in Health Insurance with an Example?

Say your plan lists a $30 copay for a primarycare visit. You schedule an appointment, arrive, and the receptionist asks for $30 before you see the doctor. After the visit, the insurer pays the rest of the approved amount maybe $120 and you owe nothing more.

Do I Have to Pay a Copay for Every Visit?

Not always. Preventive services (annual physicals, vaccinations) are often $0. Some telehealth platforms waive the fee for the first few visits. However, most specialist appointments, urgentcare trips, and prescription fills will trigger the copay.

What Happens If I Cant Pay My Copay?

A missed copay can lead to a delayed claim, a denied service, or a bill sent to collections none of which feel great. Many insurers offer a grace period, and some have patientassistance programs that can reduce or postpone the payment. Its always worth calling the member services line; a quick conversation can often prevent a nasty surprise.

Is a Copayment the Same as a CoPay in Medical Billing?

Yes. Copayment, copay, and copay are interchangeable terms. In medical billing lingo, the phrase simply denotes the fixed amount the patient pays at the time of service.

Can I Negotiate My Copayment Amount?

Directly negotiating a copay isnt typical, but you can influence it when you choose a plan during open enrollment. Selecting a plan with a higher monthly premium often yields lower copays, and viceversa. If youre selfemployed, you can shop multiple carriers to find the sweet spot that matches your healthcare usage.

Pros & Cons

Benefits of a Predictable Copayment Amount

Predictability is the biggest perk. You know youll hand over $20 for a doctors visit, regardless of the diagnosis. That helps you budget monthtomonth, prevents surprise bills, and often encourages you to seek care early rather than postponing because you fear hidden costs.

Risks & Drawbacks

On the flip side, a flat copay can feel expensive if you need frequent care. For chronic conditions, those little amounts add up fast.

Illustrative Scenario: Chronic Condition

Mike has Type2 diabetes and sees his endocrinologist monthly. His plans specialist copay is $40. Over a year, thats $4012=$480 a notable chunk of his outofpocket spending.

Mitigation Tips (Expert Advice)

- Take advantage of $0 preventive visits.

- Ask your doctor about bundled appointments (e.g., labs and consult in one visit) to reduce the number of copays.

- Consider a plan with a higher premium but lower copays if you anticipate many visits.

Find Your Copay

Reading Your Insurance Card & Member Portal

The easiest place to spot your copayment amount is right on the front of your insurance card. Look for rows labeled Primary Care, Specialist, or Prescription. If you prefer a digital view, log into your insurers portal most platforms have a Plan Summary page that lists every copay tier.

Ask Your Insurer or HR Benefits Team

A short phone call can clear up confusion. Try this script: Hi, Im reviewing my benefits and wanted to confirm the copayment amounts for primary care and specialist visits under my current plan. Most representatives will read the numbers straight from the system.

CrossChecking with the Explanation of Benefits (EOB)

After any claim, youll receive an EOB that breaks down what the insurer paid and what you owe. Look for the line item that says Copay $XX. If the amount doesnt match whats on your card, it could be a billing error or a plan change follow up quickly.

Conclusion

The copayment amount is the steady, predictable slice of each healthcare bill that lands in your lap a small but essential piece of the larger insurance puzzle. By knowing how it differs from deductibles, coinsurance, and outofpocket maximums, you can budget smarter, avoid surprise fees, and make informed choices about which plan fits your lifestyle.

Take a few minutes today to peek at your insurance card, fire off a quick call to HR, or log into your member portal. The clearer you are about your copay, the more confident youll feel navigating the healthcare maze. Got a story about a copay surprise (good or bad)? Share it in the comments wed love to hear how youve cracked the code on your healthcare costs!

FAQs

What is a copayment amount?

A copayment amount is a fixed dollar fee you pay each time you receive a covered health‑care service, such as $20 for a doctor visit.

When do I usually pay the copayment?

Most plans require you to pay the copay at the point of service—when you check in at the clinic or when the pharmacist rings up a prescription.

How does a copayment differ from a deductible?

A deductible is the total amount you must pay before insurance starts covering costs, while a copayment is the set fee you pay for each individual service after the deductible is met.

Can copay amounts be waived?

Yes. Many insurers waive copays for preventive services like flu shots, annual physicals, and certain vaccinations.

How can I find my specific copayment amounts?

Check the front of your insurance card, log into your member portal, or call your insurer’s customer service for a quick confirmation.