Ever wondered exactly how many years you might have left based on solid statistics, not just a vague guess? The answer is right here, and you dont need a PhD to understand it. In the next few minutes well walk through what an actuarial tables life expectancy calculator is, why its the most reliable tool out there, and how you can use it to make smarter decisions about retirement, insurance, and even daily health choices. Grab a coffeelets dive in together.

Why Use It

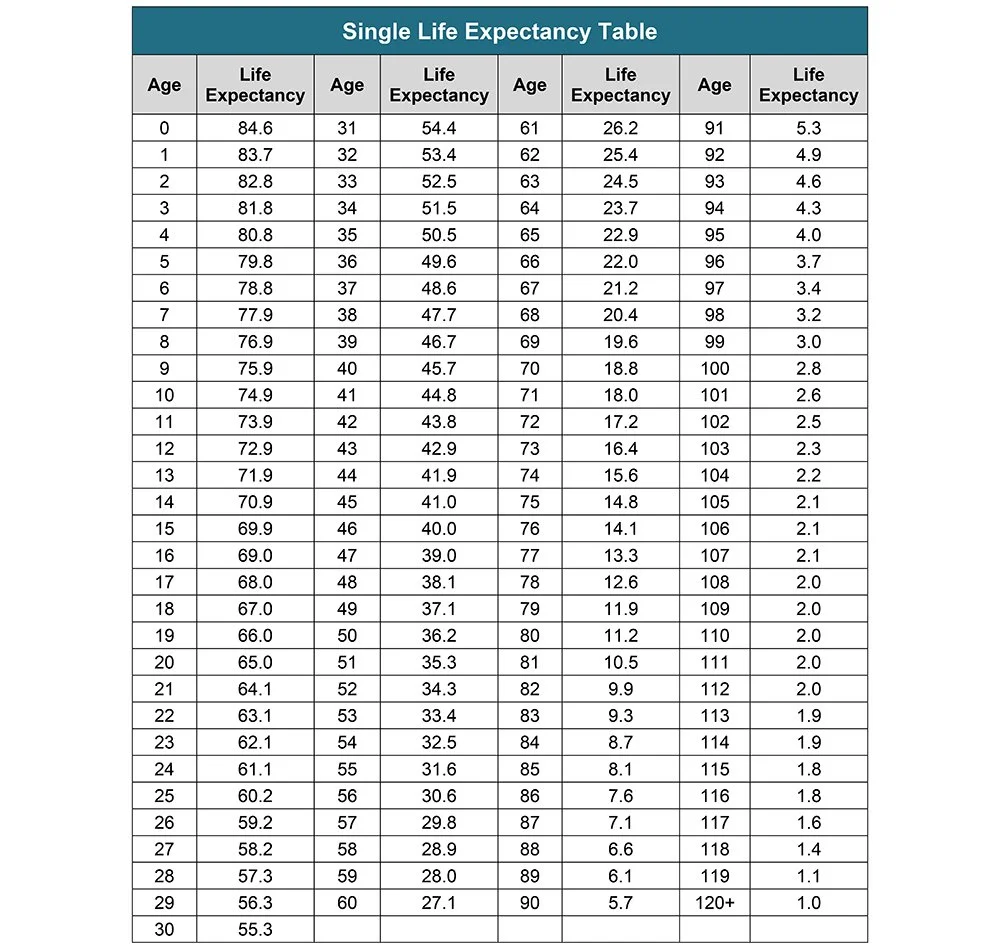

What is an actuarial table?

Think of an actuarial table as a giant spreadsheet that insurers, governments, and pension funds have been finetuning for decades. It records how many people of a certain age, gender, and sometimes other factors, are expected to survive each subsequent year. In other words, its the statistical backbone behind everything from lifeinsurance premiums to Social Security benefits.

How does it differ from free or medicalhistory calculators?

Most free life expectancy calculators you find online simply ask for your age and maybe your gender. They might be fun, but they rarely tap into the deep, governmentbacked data that actuarial tables provide. Tools based on medical historylike those offered by some insurersadd layers such as smoking status, BMI, and blood pressure. Those calculators can feel more personal, yet they still lean on the same core mortality tables for their baseline numbers.

Comparison Snapshot

| Tool | Data Source | Inputs Required | Cost |

|---|---|---|---|

| SSA Actuarial Calculator | U.S. Social Security Administration tables | Sex, date of birth | Free |

| John Hancock HealthLinked | Private insurer tables + health questionnaire | Sex, DOB, BMI, smoking, etc. | Free (with enrollment) |

| Longevity Illustrator (SOA) | Society of Actuaries research | Sex, DOB, health factors | Paid subscription |

Notice the tradeoff: the SSA tool is the most accurate life expectancy calculator for pure statistical estimates, while healthlinked calculators give a personalized spin but depend on the quality of your selfreported data.

How It Works

Input variables required

At its simplest, the calculator needs just two pieces of information: your gender and your date of birth. Some premium versions ask for additional health metricsweight, height, smoking status, and chronic conditions. Those extra fields can shift the result a few years up or down, but the underlying calculations still stem from the same actuarial tables.

What the output really means

When the calculator tells you, you have 22.4 years remaining, its giving you a period life expectancy. Thats the average number of additional years a person of your exact age and gender would live if the mortality rates of todays population applied forever. Its not a prediction of your exact death dateits a statistical average.

Stepbystep walkthrough

Lets run through the official SSA calculator together. First, head to the . Youll see fields for gender and birth date. After you hit Calculate, the page shows something like average additional years: 23.5. Add that to your current age, and you have an estimated age at death. Easy, right?

Common misconceptions

- It predicts the exact day Ill die. Nope. Its a populationlevel average.

- It ignores my health conditions. The baseline table doesnt, but many calculators let you layer health factors on top.

- Its only for retirees. Actually, you can use it at any age to inform insurance needs, estate planning, or lifestyle goals.

Choosing Accurate Tool

What makes a calculator most accurate?

A most accurate life expectancy calculator leans on the freshest actuarial tablesusually updated annually by government agencies or professional societies. It also shows you the source of its data, so you can verify the methodology. Transparency is a big trustbuilder.

Free vs. paid options

The free SSA calculator is a solid baseline. If you want a free tool that also asks about medical history, look for calculators that advertise life expectancy calculator based on medical history free. They can be handy but remember theyre still built on the same core tables. Paid toolslike the often provide deeper scenario analysis, customized reporting, and uptodate research.

Pros/Cons Checklist

- SSA Free Calculator: Completely free, official data, minimal inputsgreat for quick checks.

- HealthLinked Free Calculators: More personalized, but may overemphasize selfreported data.

- Paid Professional Tools: Detailed projections, scenario planning, but require a subscription.

How to validate a calculators credibility

Look for citations to the Social Security Administration, the Society of Actuaries, or other recognized actuarial bodies. A trustworthy site will often have an About the data page that explains which tables they used and when they were last updated. If you cant find that info, its a red flag.

Practical Applications

Retirement planning

Knowing your estimated remaining years helps you size up Social Security benefits, pension payouts, and the longevity of your retirement portfolio. For example, if the calculator says you have 25 years left, youll likely need a longer drawdown strategy than if it says 18 years.

Estate & legacy planning

Life expectancy drives how much life insurance you should buy, how you structure trusts, and the timing of charitable gifts. A higher life expectancy often means a larger insurance need to protect your heirs.

Healthandwellness goalsetting

Seeing a concrete number can be a motivator. If your result is lower than you hoped, you might decide to quit smoking, adopt a regular exercise routine, or schedule that overdue checkup. Its a gentle nudge toward healthier choices. For people managing chronic conditions such as IBS, pairing lifestyle changes with medical guidance can improve quality of life and may influence longevity estimates; for practical tips on dietary timing and symptom management see intermittent fasting IBS.

Realworld case study

Meet Sarah, a 55yearold accountant. She ran the SSA calculator and got an additional 22.7 years estimate, putting her expected age at death at 77.6. Armed with that, she increased her 401(k) contributions, bought a levelpremium lifeinsurance policy, and started a weekly walking group. Six months later, she feels more in control of her futurejust because a simple number sparked a cascade of proactive steps.

Limitations & Risks

Statistical averages vs. individual variance

Remember, actuarial tables are averages across thousands of people. Your personal risk factorsgenetics, lifestyle, environmentcan shift you above or below that average. Thats why the calculator is a guide, not a verdict.

Data lag & demographic shifts

Tables are updated periodically, but medical breakthroughs or sudden publichealth events (think pandemics) can make past data less reflective of the present. Always treat the number as a moving target, not a static fact.

Potential misuse

Some people use lifeexpectancy numbers to make drastic financial decisions without consulting a professional. That can backfire. The safest route is to pair the calculators output with advice from a physician and a certified financial planner.

Balanced advice tip

Use the calculator as a starting point, then get a health checkup to finetune the estimate, and finally meet with a planner to translate those numbers into concrete strategies.

StepbyStep Guide

Ready to try it yourself? Follow these simple steps:

- Visit the .

- Select your gender and type in your birth date (formatMM/DD/YYYY).

- Click Calculate. The page will display average additional years.

- Add that figure to your current age. Thats your projected age at death.

- Save the resultmany planners ask for this number when you discuss retirement or insurance.

Tips for accurate input

- Doublecheck the birthdate format; a transposed digit can shift the result by years.

- Choose the correct gender optionsome tools also offer a nonbinary option that maps to the average of male and female tables.

- If the tool asks for health metrics, be honest. Overoptimistic inputs can give a falsely high estimate.

Visual aid (suggested for final article)

Consider adding a screenshot of the SSA input screen with arrows pointing to the key fields. It helps visual learners follow along without confusion.

Conclusion

Using an actuarial tables life expectancy calculator gives you a datadriven glimpse into how many years you might have left, grounded in official government tables. Its more reliable than a quick Google search, and when you layer in health data or professional advice, it becomes a powerful compass for retirement, insurance, and wellness decisions. So go aheadrun the SSA calculator today, note the number, and let it spark a thoughtful conversation with your doctor or financial planner. Your future self will thank you.

FAQs

What is an actuarial tables life expectancy calculator?

An actuarial tables life expectancy calculator uses official mortality data to estimate how many more years a person is expected to live based on age and gender.

How accurate is an actuarial tables life expectancy calculator?

These calculators are highly accurate for population averages but can't predict individual outcomes due to personal health and lifestyle factors.

Can I use an actuarial tables life expectancy calculator for retirement planning?

Yes, these calculators help estimate how long retirement savings need to last and guide decisions about Social Security and pension benefits.

Do actuarial tables life expectancy calculators consider health conditions?

Basic calculators use only age and gender, but some advanced tools allow input of health factors for a more personalized estimate.

Where can I find a reliable actuarial tables life expectancy calculator?

The Social Security Administration and the Society of Actuaries offer trusted actuarial tables life expectancy calculators online.